Unlock Your Potential: How Instant Payments Can Power Innovation

Instant payment services are a key feature for enterprises seeking to upgrade their payment operations. Supporting instant payment options helps to increase customer retention and satisfaction rates, reduce costs, improve cash flow and minimize payment disruptions. This can create a frictionless payment ecosystem for enterprises and customers.

In this guide, we'll show you how to unlock your competitive advantage with instant payments.

Alternative Payment Methods and the Evolving Payments Landscape: Why Innovation Matters

The financial services sector is experiencing unprecedented pressure to accelerate digital payment processing in response to evolving consumer and business expectations.

Conditioned by mobile commerce and digital experiences that deliver immediate results, today’s consumers are setting the standards. From instant messaging to same-day delivery, consumers expect transactions to happen in real time. Whether they're receiving wages, making purchases or transferring money to other accounts, consumers increasingly view multi-day payment processing as outdated and inconvenient.

Enterprise payment needs mirror consumer expectations but with additional complexity. While B2B transactions involve larger budgets, more stakeholders and longer decision-making processes, businesses are equally frustrated by payment delays that impact cash flow, supplier relationships, customer satisfaction and operational efficiency.

In fact, slower payment methods, like checks, have been declining in recent years and are being replaced by faster alternatives like ACH payments. However, even traditional ACH processing—which can take 1-5 business days—is no longer meeting the speed requirements of modern business operations.

As both consumers and businesses seek alternatives to slow, expensive payment methods, account-to-account (A2A) payment technology has emerged as the solution. Companies that recognize and act on the demand for faster payments can differentiate themselves through superior payment experiences, improved cash flow management and enhanced customer satisfaction.

Instant payment technology sits at the center of this transformation, offering enterprises a direct pathway to meet the speed expectations of both their customers and their own operations—without the delays and limitations of traditional payment methods.

Unpacking Instant Payments: The Foundation of Modern Transactions

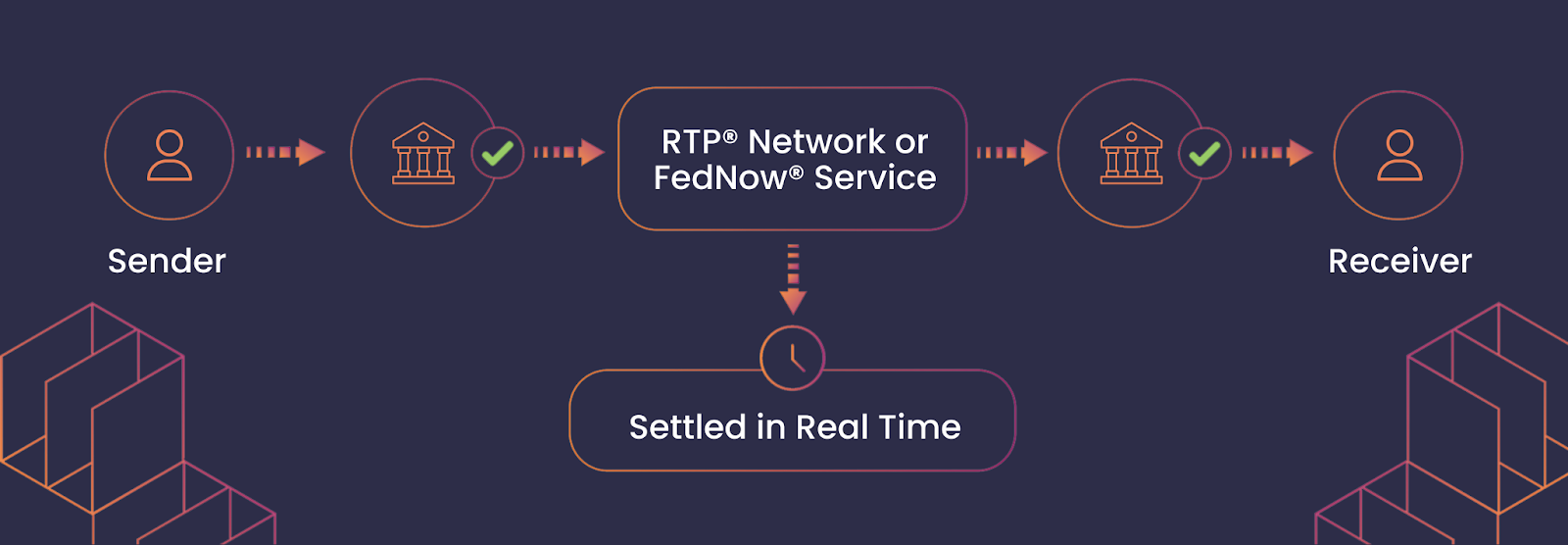

Instant payments represent a paradigm shift from traditional fund transfer methods. These systems enable money movement that typically completes within seconds rather than requiring the multi-day settlement periods associated with conventional approaches.

The United States utilizes two major instant payment infrastructures that power this transformation:

- The Clearing House operates the RTP® network, which launched in 2017 and has established itself as a leader in real-time transactions. Recent performance data shows the network processed 98 million transactions valued at $80 billion in the last quarter of 2024, with participating financial institutions growing by 67%.

- Launched in July 2023, the Federal Reserve's FedNow® Service represents the newest entrant to the instant payments market. The service has rapidly gained adoption, with more than 1,000 participating financial institutions and 37 payment providers processing 1.5 million transactions throughout 2024.

Both systems enable faster, more efficient transactions that benefit individuals and businesses alike by allowing them to send and receive funds within seconds, 24/7/365. This availability represents a significant advancement over standard ACH processing, which typically requires 1-5 business days to process payments.

Pay-by-bank transfers, powered by these instant payment rails, are gaining significant traction. Projections estimate real-time transactions will reach more than $575 billion globally by 2028 and account for more than 27% of all electronic payments. This growth demonstrates the mounting demand for secure, cost-effective alternatives to traditional payment methods.

What is an Instant Payments API?

APIs are the language that connects today's pay-by-bank payments. They reduce technical and operational costs, enabling business owners to focus on their core product or service.

Juniper Research estimates global banking-as-a-service platform revenue will reach $94 billion by 2028, an increase of 158% from the $36.4 billion valuation in 2024. Payments APIs help to facilitate this growth, bridging gaps to provide businesses with payment processing options and efficiency they wouldn't have access to otherwise.

Through APIs, businesses can tap into RTP and FedNow to enable instant payments that provide more integrated customer experiences.

Payments APIs also help facilitate better overall payment performance, making business payment processing more efficient and flexible without each business building the infrastructure from scratch. As a result, businesses can reduce the time it takes to launch a product or service and realize revenue more quickly. Now that customers demand near-immediate gratification, payments APIs allow companies to adopt a fast and global approach.

In addition to market agility, payment APIs are future-proofing tools. Every business that wants to grow and continue transacting in the digital world needs to provide fast and secure payment processing. APIs help businesses stay current with the payment landscape as it changes and maximize the interoperability of the global financial system.

Understanding ISO 20022

Instant payments in the United States are built on the ISO 20022 messaging standard, a revolutionary protocol that fundamentally transforms how payment data is structured and transmitted.

This advanced messaging standard allows instant payments to carry significantly more contextual information than traditional payment methods. Where conventional ACH transactions might include only basic routing and account details, ISO 20022-powered instant payments can include comprehensive remittance data, detailed transaction purposes and structured business information that travels with the payment in real time.

The enhanced data capabilities of ISO 20022 provide unprecedented transparency into payment flows. Businesses can access detailed information about transaction origins, purposes and recipients, enabling more sophisticated reconciliation processes and reducing the manual effort typically required to match payments with invoices or orders. This structured data approach also facilitates automated processing and reduces errors that commonly occur with manual data entry or interpretation.

For enterprises, this means instant payments don't just move money faster—they move information quickly and more accurately, creating opportunities for streamlined operations and improved financial visibility that weren't possible with traditional payment rails.

API-Powered Data Visibility and Payment Tracking

Building on the rich data foundation provided by ISO 20022, many modern payments APIs further enhance data visibility and tracking capabilities. These APIs serve as the bridge between the structured data of instant payments and business applications, enabling real-time access to comprehensive payment information.

Enhanced Remittance Data: APIs can capture and transmit the detailed remittance information supported by ISO 20022, allowing businesses to include invoice numbers, purchase order references and other critical business context directly within the payment. This eliminates the need for separate remittance advice and enables automatic reconciliation processes.

Correlation IDs for End-to-End Tracking: Payment APIs provide correlation ID functionality that acts as a unique identifier throughout the entire payment lifecycle. Whether it's an invoice number, order confirmation or business-specific UUID, this tracking capability allows businesses to monitor payments from initiation through completion, much like tracking a package through delivery.

Real-Time Status Updates: Webhooks and API notifications deliver instant updates on payment events, providing businesses with immediate visibility into payment approvals, failures or status changes. This real-time feedback enables dynamic business processes and responsive customer experiences.

Comprehensive Analytics and Insights: With access to both ISO 20022's structured data and API-driven tracking capabilities, businesses gain deeper insights into their payment operations. They can identify transaction trends, monitor payment performance across different channels, detect and manage suspicious activity, and discover strategic growth opportunities through comprehensive data analysis.

This combination of ISO 20022's structured messaging and API-enhanced tracking creates a powerful foundation for payment innovation, enabling businesses to build more intelligent, responsive and efficient payment processes that leverage real-time data for competitive advantage.

What are Instant Payments Use Cases?

These use cases from multiple industries demonstrate the potential with digital payments.

- Buy Now Pay Later (BNPL): Enable instant disbursements to merchants at the point of purchase using real-time payment rails, providing immediate settlement instead of traditional multi-day ACH processing. BNPL providers can instantly transfer funds to retailers when customers make purchases, creating seamless checkout experiences with real-time payment confirmation. Instant payments also enable immediate repayment processing that automatically updates customer account balances and available credit limits when payments are received.

- Insurance: Accelerate claims processing with instant insurance payouts directly to policyholders' bank accounts. Eliminating the delays associated with paper checks also helps enhance customer satisfaction.

- Supply Chain: Revolutionize supplier payments with instant disbursements. By bypassing the check deposit process, businesses can optimize cash flow and strengthen supplier relationships.

- Real Estate: Streamline real estate transactions with instant fund transfers. From earnest money deposits to closing day disbursements, instant payments help create a seamless and efficient process.

- Healthcare: Modernize healthcare payments with instant claims reimbursement. Reduce administrative costs and improve patient experiences by eliminating the need for paper checks.

Across industries, instant payments play a vital role in an enterprise’s digital transformation journey.

What Should My Business Consider Before Adopting Instant Payments?

Before implementing instant payments, enterprises must carefully evaluate several critical operational and strategic factors that significantly differ from traditional payment processing:

24/7/365 Operational Readiness

Instant payments operate continuously, including weekends, holidays and after traditional banking hours. This requires businesses to assess whether their payment operations, customer support teams and internal systems are prepared to handle payment activity around the clock. Consider whether your organization has the staffing, monitoring capabilities and operational procedures necessary to manage payments that can occur at any time.

Enhanced Fraud Protection for Continuous Operations

The irrevocable nature of instant payments, combined with their 24/7 availability, demands robust fraud prevention measures that can operate effectively at all times. Traditional fraud monitoring systems designed for business-hour operations may need significant upgrades to handle suspicious activity detection during off-hours when human oversight is limited. Investing in advanced automated fraud detection systems becomes essential for these payment types.

Dispute Management for Irrevocable Transactions

Unlike traditional payment methods that may allow for reversals or chargebacks, instant payments are final once processed. Businesses must establish clear procedures for handling customer disputes surrounding claims of unauthorized payments. This includes implementing strong customer authentication processes upfront, maintaining detailed transaction records and developing customer service protocols specifically designed for irrevocable payment disputes.

Network Connectivity Strategy

Enterprises must decide whether to connect to the RTP network, the FedNow Service or both systems. Since these networks aren't interoperable, businesses connecting to both should consider investing in intelligent routing capabilities to determine recipient bank eligibility and select the appropriate network for each transaction. This decision impacts your potential reach, as different financial institutions participate in different networks.

Build Versus Buy Decision

Organizations face a fundamental choice between developing instant payment connections internally or partnering with technology providers who already maintain network connectivity. Building direct connections requires significant technical resources, ongoing maintenance and expertise in payment system integration. Alternatively, working with experienced payment service providers can accelerate implementation while providing access to established infrastructure, compliance frameworks and ongoing support.

Each of these considerations requires careful planning and may significantly impact your implementation timeline, resource requirements and operational procedures. Successful instant payment adoption depends on comprehensively addressing these factors before launching the service.

The Engine of Speed: How Real-Time Payment Processing Works

Real-time payment systems operate on advanced infrastructure designed for immediate transaction processing between financial institutions. This technology eliminates the batch processing limitations that characterize traditional payment methods, enabling continuous operation regardless of time or day.

The challenge for businesses lies in network fragmentation. Financial institutions have adopted different instant payment services—some participate in the RTP network, others in FedNow and many in both systems. However, universal coverage and interoperability between RTP and FedNow doesn't yet exist, creating potential gaps in payment reach.

Embracing Payment Orchestration Platforms

Intelligent payment routing technology addresses this complexity by automating rail selection for each transaction. Payment orchestration platforms analyze multiple factors—including recipient bank capabilities and business preferences—to determine the optimal processing path.

Dwolla's orchestration technology eliminates the burden of managing multiple payment rails manually. The platform performs real-time eligibility verification and automatically selects the most effective path for routing transactions. This happens transparently, presenting businesses with a unified payment interface while maximizing transaction success rates and network reach.

Implementing Instant Payments: A Strategic Guide for Enterprises

For enterprises ready to leverage the benefits of instant transfers, the implementation process doesn't need to be overwhelming. Partnering with an experienced payment service provider offers the most direct path to success.

A payment API serves as the bridge between your business operations and the broader financial system. There are multiple payment providers on the market, but the right provider will offer comprehensive documentation, developer resources and support throughout the integration process. This collaborative approach ensures your instant payment implementation aligns with your business objectives and technical requirements.

By partnering with Dwolla, enterprises have access to an orchestration solution capable of automatically determining the right instant payment rail for each transaction, maximizing reach and efficiency without requiring businesses to manage the underlying complexity. This enables enterprises to focus on their core operations while delivering a superior payment experience to their customers and partners.

Key Considerations for Success: Mitigating Risk and Maximizing Impact

Successful instant payment implementation requires careful attention to several critical factors:

Security First: The irreversible nature of instant transactions demands robust payment fraud prevention measures implemented at the transaction initiation point. Advanced security systems utilizing artificial intelligence and machine learning technologies can identify and prevent suspicious activity before funds are transferred. Early implementation of comprehensive fraud detection helps create a secure foundation for the entire payment landscape.

Reach and Coverage: Given the multi-rail structure of the U.S. instant payments market, enterprises benefit from partnering with providers that maintain connectivity to both major networks. This comprehensive access helps provide maximum payment coverage and the ability to reach the broadest possible range of customers and business partners.

Operational Efficiency: An instant payments integration should streamline rather than complicate existing business processes. Effective solutions provide automated capabilities for bank eligibility verification and payment routing between instant payment networks, reducing the need for manual intervention and oversight.

Customer Experience: Customers should encounter consistent, intuitive experiences regardless of which underlying payment infrastructure processes their transaction. Reliable status communications, real-time notifications and clear confirmation processes build user confidence and satisfaction.

Internal Controls & 24/7 Operations: Organizations must adapt their operational procedures and control frameworks to accommodate round-the-clock payment processing. This adaptation encompasses fraud monitoring capabilities, customer support availability, back-office reconciliation workflows and comprehensive operational preparedness for continuous transaction activity.

The Enterprise Impact: Fueling Growth and Efficiency with Instant Payments

The increased speed provided by instant payments, combined with the ability to process payments anytime, provides numerous benefits for both consumers and businesses.

Benefits of RTP and FedNow include:

- Fast Settlement: Users' transactions move at the same fast-paced speed they're used to from other tech rather than facing multi-day delays.

- Improved Cash Flow: Businesses can improve their cash flow by more easily collecting payments from customers and suppliers, which can be especially helpful for businesses that operate in industries where timely payments are critical, such as e-commerce or the gig economy.

- Improved Liquidity Management: Instant payments give businesses a more accurate view of their cash flow so they can make better decisions about how to allocate their resources.

- Enhanced Customer Experience: Instant payments can provide a more convenient and efficient way to make payments. For example, insurance companies can improve the reimbursement experience for policyholders by processing instant insurance claim disbursements. In real estate, instant payments may offer cost-effective alternatives to wire transfers that can process transactions with greater speed and visibility. In the gig economy, workers can receive immediate compensation.

- Increased Transparency: Transactions can have detailed remittance data attached to them using ISO 20022, which helps businesses track and reconcile payments more easily.

Improving payment flows translates into tangible business outcomes: reduced costs, increased revenue opportunities and enhanced customer loyalty—all contributing to sustainable competitive advantages in an increasingly dynamic marketplace.

Dwolla: Your Partner in Payments Innovation - Instant Payments, Powered Intelligently

The continued expansion of instant payment capabilities requires enterprises to partner with experienced technology providers who understand the complexities of modern payment infrastructure. Dwolla's payment platform delivers integrated access to both major U.S. instant payment networks through a single API connection, eliminating the technical challenges typically associated with multi-network integration.

Dwolla's pay-by-bank solutions enable businesses to implement open banking principles for enhanced security and reduced costs compared to traditional payment methods. When combined with instant payment functionality, these capabilities provide enterprises with powerful tools for payment strategy optimization.

The future of payments is instant, intelligent, and integrated. By partnering with Dwolla, enterprises can position themselves at the forefront of this transformation, unlocking new levels of operational efficiency and customer satisfaction.

Learn how Dwolla can empower your enterprise with cutting-edge instant payment capabilities and intelligent orchestration solutions to fuel sustainable growth in the modern payments ecosystem.